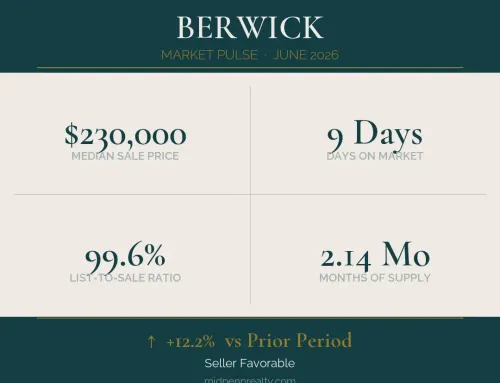

Montgomery, PA 17752 Real Estate Market Report | April 2026

Montgomery, PA 17752 Real Estate Market Report | April 2026

The most telling detail in Montgomery’s April 2026 market data is not the price trend or the days on market. It is the relationship between what sellers are asking and what buyers are actually paying.

The median list price in the 17752 ZIP code currently sits at $179,250. The median sale price is $134,000. That is a meaningful gap, and it tells a more nuanced story than a simple price decline might suggest on its own. Markets where that spread is wide are often markets in transition, where seller expectations and buyer willingness have not yet reached full agreement. Understanding how that gap formed, and what it means for both sides of a transaction, is where the real value of this report lies.

Montgomery is a small borough in Lycoming County, situated along the West Branch of the Susquehanna River and Route 405, roughly equidistant between Williamsport to the north and Sunbury to the south. It is a community where affordability has historically been a primary draw, with modest residential inventory, a working-class character, and proximity to employers in both Lycoming and Northumberland counties. The real estate market here is small by volume, which means individual sales can move the needle significantly in either direction on any given month.

With that context in mind, here is what the April 2026 data is showing.

There are currently nine active listings in the 17752 market area. That is a limited pool of homes, and in a borough the size of Montgomery, nine active listings represents meaningful supply relative to typical transaction volume. The months of supply reading of 4.5 is worth examining carefully. By conventional real estate standards, a balanced market sits at roughly five to six months of supply. At 4.5 months, Montgomery is technically on the seller-favorable side of that threshold, though it sits close enough to the center that describing it as a fiercely competitive seller’s market would be an overstatement.

The days on market figure, however, tells a different story. Homes that are going under contract are doing so in approximately 11 days. That is a fast pace by any reasonable measure. When a market with 4.5 months of supply is simultaneously producing 11-day median contract timelines, it suggests that the homes actually attracting buyers are well-positioned, either in price, condition, or both. Buyers are moving quickly when they find a home that meets their criteria, even in a market where the overall inventory level would typically give them more room to deliberate.

This brings us back to the list-to-sale price relationship. The current median list price of $179,250 against a median sale price of $134,000 represents a substantial gap of roughly 25 percent. In a typical healthy market, that spread would be far narrower, often in the range of one to three percent below list price in a balanced environment, and sometimes above list price in a highly competitive one. A gap of this size almost always indicates one of a few things: some listings are priced well above what the market will support and are either sitting longer or eventually selling at significant reductions, the homes that are closing are fundamentally different in type or condition from those that are listed but not yet sold, or both factors are at play simultaneously.

In a small market like Montgomery, both explanations are plausible. A single home listed at $250,000 or more in a neighborhood where most sales occur in the $100,000 to $150,000 range can skew the median list price considerably. Meanwhile, the homes that close quickly at or near the 11-day median are likely the properties priced realistically from the start, drawing competitive attention and reaching contract before the slower-moving inventory has a chance to resolve.

The five percent price decline compared to the prior period adds another layer to this picture. That figure reflects movement in the median sale price, not necessarily a decline in what individual homes are worth. When months of supply sits below the balanced threshold and homes are still selling in under two weeks, a softening in the median sale price often reflects a shift in the composition of what sold rather than a broad loss of value across the board. Without multi-year historical data specific to the 17752 market, it is difficult to say with certainty how this period compares to prior April readings. What can be said is that a market classified as seller-favorable, with sub-two-week contract timelines, is not typically showing the symptoms of a distressed or declining market. The pricing trend warrants monitoring, but it does not by itself signal broader deterioration.

Where historical context would be particularly valuable is in the months of supply figure. If April readings in Montgomery over the past three years consistently showed supply below two months, then 4.5 months would represent a meaningful loosening of conditions and a genuine shift in buyer leverage. Conversely, if prior Aprils regularly saw five or six months of supply, the current reading would indicate a market that is actually tighter than normal. The data to make that comparison is not available in this reporting period, but it is the question any serious buyer or seller in this market should be asking.

For buyers considering a home in the Montgomery area, the current conditions offer a more nuanced opportunity than many Central Pennsylvania markets have provided over the past few years. With nine active listings and a months of supply reading close to balanced, buyers have some real selection. They are not walking into a market where every home receives five offers on day one. That said, the 11-day days on market figure is a reminder that well-priced, well-maintained homes are not sitting. When a home in this market is priced correctly, it does not wait. Buyers who are pre-approved, clear on their criteria, and working with a knowledgeable local agent are the ones best positioned to move confidently when the right property comes available.

The wide gap between list and sale prices may tempt some buyers to open every negotiation with a deeply discounted offer. That approach can work on overpriced listings that have been sitting on the market for an extended period. It is far less likely to work on a home that hits the market priced at or near local market value. Understanding the difference between those two categories of listings is one of the most practical things a buyer can bring to this market.

For sellers, the April data offers a reasonably encouraging picture, but with important caveats. The seller-favorable classification and fast days on market are genuinely positive signals. Motivated, pre-qualified buyers are clearly active in this area. The list-to-sale price gap, however, is a clear reminder that price positioning matters more in a small market than in a high-volume one. In a borough like Montgomery, where monthly transaction counts are modest, an overpriced listing does not benefit from the sheer volume of buyer traffic that might eventually produce a contract in a larger market. It simply sits, and sitting inventory in a small market becomes visible quickly. Sellers who price their homes at a level grounded in actual recent comparable sales are far more likely to find themselves among the homes generating contracts in 11 days than among those contributing to the upper end of the list price median.

The broader picture that April 2026 paints for Montgomery, PA is one of a small but reasonably active market where motivated buyers and realistic sellers are finding each other efficiently. The conditions are not extreme in either direction. They are not the frenzied seller’s market that characterized much of the region two and three years ago, nor do they reflect meaningful buyer-side weakness. What they reflect is a community where local fundamentals, affordability, proximity to employment corridors, and genuine housing need continue to drive baseline demand, even as broader market dynamics and mortgage rate pressures create headwinds for higher-priced inventory.

The trend worth watching most closely in the months ahead is whether that list-to-sale price gap narrows. If it does, it will likely mean that seller expectations are adjusting toward market reality, which would indicate a healthier, more fluid transaction environment. If it widens, it may suggest that pricing pressure is building and that the market is gradually tipping toward buyers even in the face of limited inventory.

If you would like to receive the complete Mid Penn Market Pulse report for the Montgomery and Lycoming County market area, including detailed local data and ongoing trend monitoring, you can sign up for the full report at Mid Penn Realty’s market report page. Having that information updated regularly puts you in a better position to make decisions grounded in what the market is actually doing, not what it was doing six months ago.